Until very recently, the hefty monetary and fiscal relaxation unleashed by governments to stimulate the economic recovery at the onset of the global financial crisis has not had major inflationary repercussions, in particular as the main benchmark has been the benign consumer price inflation, rather than the rapidly growing real-estate and stock-exchange prices. At the same time, the so-called modern monetary theory has grown very popular with both academics and market analysts. The theory wrongly claims that governments on fiat currency can afford to monetize large budget deficits without fear of negative economic consequences. Inflation concerns have been brushed aside as highly unlikely and easy to be solved by subsequent policy measures. Japan has been the preferred example of modern monetary theory advocates due to its low inflation despite massive growth stimuli. Yet, given its specific conditions, Japan is a misleading case and the economies which emulated its policies are now faced with fast-rising consumer prices.

Japan’s Senseless Struggle with Deflation

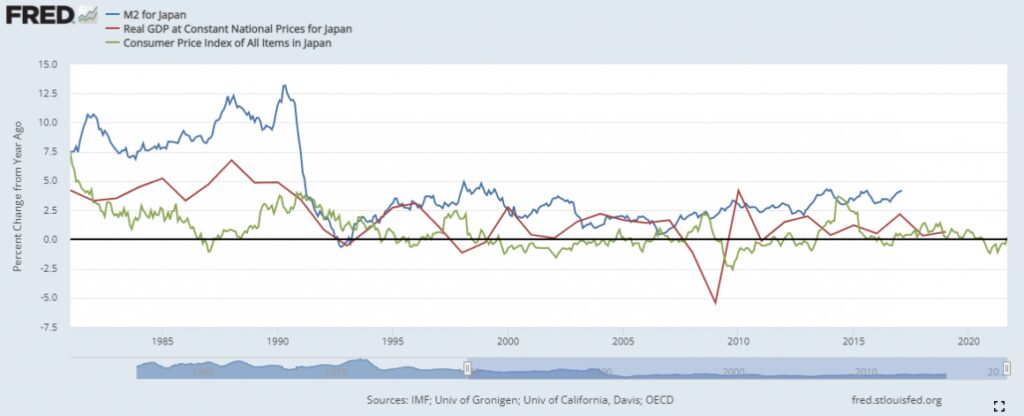

Soon after the collapse of its asset price bubble in the early 1990s, Japan entered a prolonged period of anemic growth and low inflation with short spells of deflation (graph 1). Instead of letting prices readjust and a curative recession purge the boom’s malinvestments—as advocated by the Austrian theory of the business cycle—the government engaged in massive fiscal and monetary stimuli over three decades. Japan tried to spur sluggish demand with a Keynesian program of public works and large budget deficits peaking at above 10 percent of gross domestic product in 1998 and 2009. In parallel, public debt soared almost four times, from 63 percent of GDP in 1990 to a whooping 235 percent of GDP in 2019, monetized to a large extent by the central bank. Needless to say, economic growth has been disappointing.

Graph 1: Japan’s real GDP, consumer price index, and M2 money supply evolution

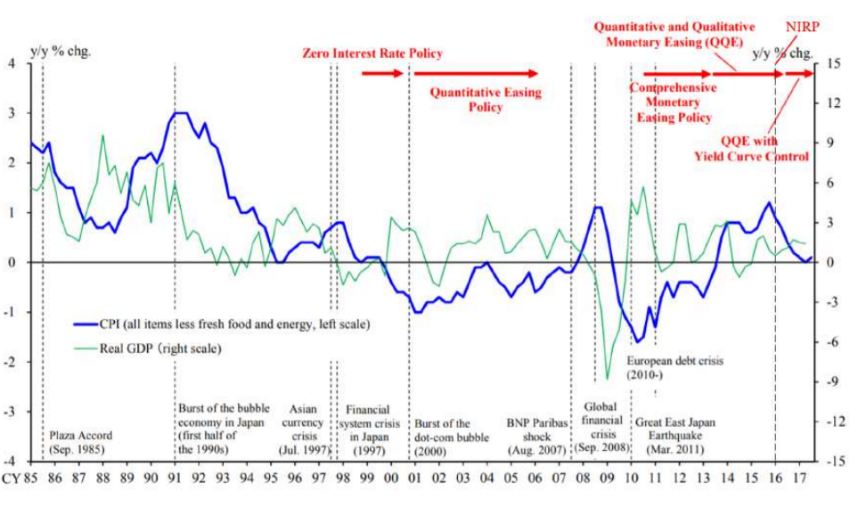

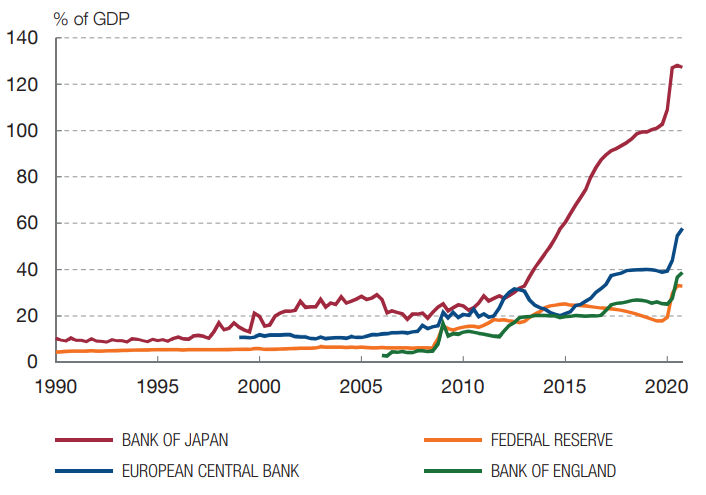

The Bank of Japan (BoJ) embarked on a series of unconventional policy measures early on (IMF 2020). In 1999–2001, it became the first among major economies to experiment with zero interest rate policy and introduced quantitative easing about the same time (graph 2). In 2013/2014, the BoJ sharply increased its purchases of Japanese government bonds and risky assets through quantitative and qualitative easing, and surprised market participants in early 2016 with negative interest rates for a portion of banks’ reserves. In September 2016, the BoJ initiated a new program, yield curve control, in order to raise inflation expectations. It started buying government bonds along the entire yield curve with a 0 percent target for the ten-year yield and committed to allowing inflation to “overshoot” the 2 percent target. As a result of this monetary expansion experiment, the BoJ’s balance sheet surged from around 30 percent of GDP in 2013 to above 120 percent of GDP in 2019 and its holdings of Japanese government bonds reached a staggering 90 percent of GDP in March 2020 (graph 3).

Graph 2: Japan’s history of monetary easing

Graph 3: Balance sheet size: Bank of Japan versus other central banks

Japan’s Conditions Were Very Specific

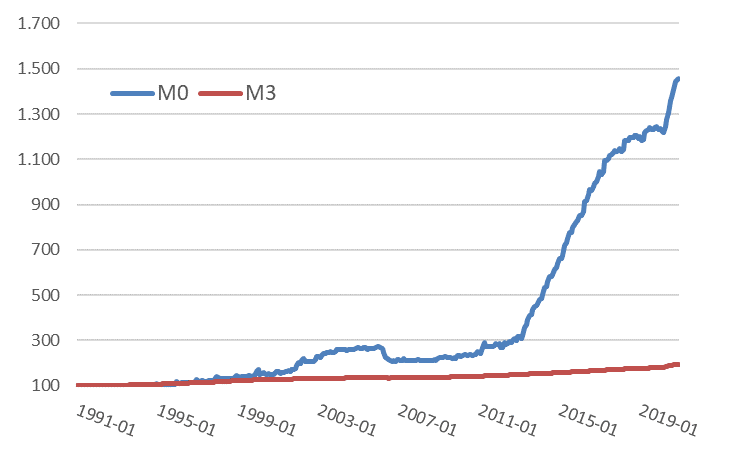

The reasons why Japan’s decades-long monetary relaxation has not translated into higher consumer price index inflation are different from what mainstream economists have thought. First, as Rothbard explains, the crisis that follows a credit boom is accompanied by a contraction of the money supply, which together with an increase in the demand for money prompts an adjustment to lower prices. Far from being detrimental to recovery, it leads to a larger price differential, i.e., a higher “natural” rate of interest between stages of production, which accelerates the cleanup of malinvestments and rebuilding of savings. Although the Japanese authorities did their best to avoid deflation and a curative recession, their actions have only managed to keep zombie companies and banks alive, which prolonged the recession and misallocation of factors of production. Yet they were not able to reengineer another boom or meet the 2 percent inflation target because the credit multiplication mechanism and monetary transmission channel were obviously impaired. Graph 4 shows the massive growth differential between the monetary base under the control of the central bank and the broad money supply determined primarily by lending activity.

Graph 4: Japan’s monetary base (M0) and broad money (M3)

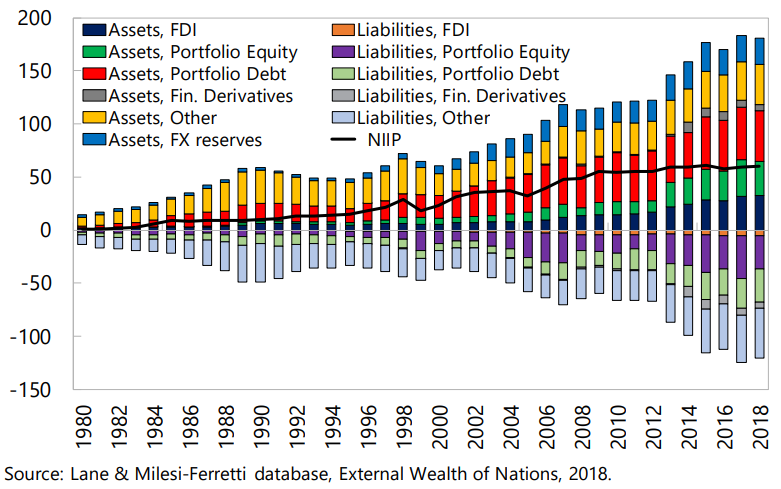

Second, the impact of the BoJ’s aggressive monetary easing was dampened by hefty capital outflows triggered by the low-yield environment and worsening domestic economic conditions. Although mainstream pundits claim that adverse demographics and deflation are the root cause of Japan’s lost decades, in reality pernicious government policies are to be blamed (Macovei 2020). As unprofitable companies were kept afloat, wasting scarce resources and labor and raising production costs for all businesses, viable firms moved capital and investments abroad. In less than four decades, Japan has accumulated the largest net international investment position in the world at about $3 trillion, or 60 percent of GDP (graph 5). During the last two decades alone, Japan’s net international investment position surged by the equivalent of ¥225 trillion. Had this amount been invested in Japan, the broad money supply would have increased by 75 percent instead of about 50 percent over this period, with a corresponding effect on domestic prices.

Graph 5: Japan’s net international investment position as a percentage of GDP

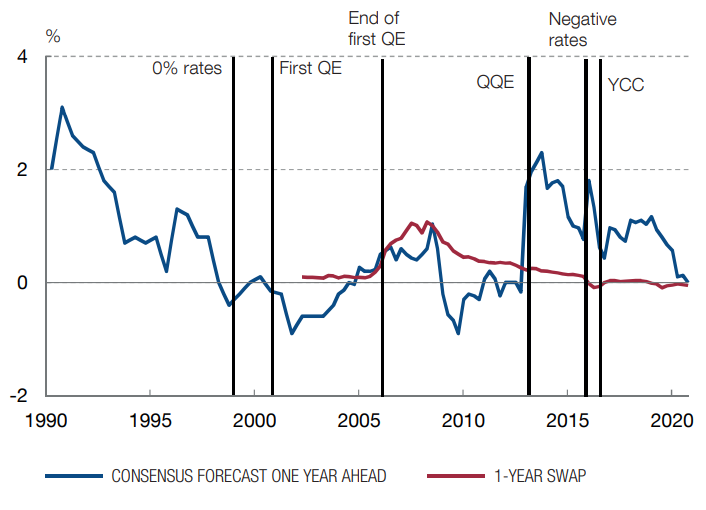

Third, inflation expectations, in particular short-term ones, remained subdued and very much in line with actual inflation despite highly expansionary fiscal and monetary policies (graph 6). Woes caused by the tarrying economic recovery, the bankruptcies of financial institutions, and concerns about the fragility of the domestic financial system in general led to a decline in inflation expectations except for a short-lived spike at the beginning of Abenomics.

Graph 6: Short-term inflation expectations

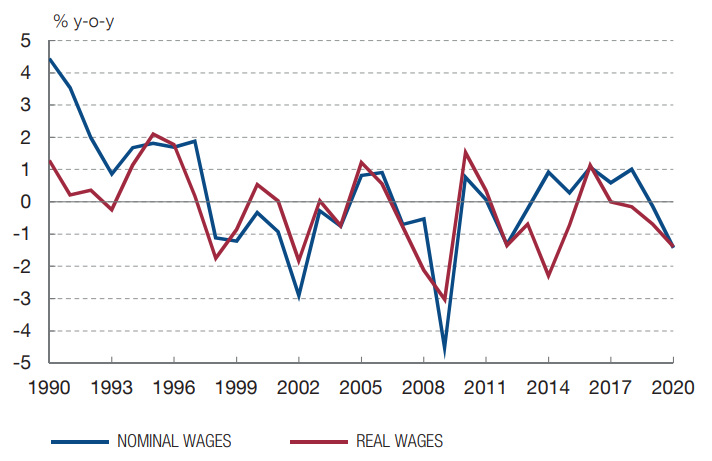

In addition, Japan’s inflation expectations have been largely shaped by past inflation, leaving inflation targets a smaller role to play. This distinguishes Japan from other advanced economies, including the US, and reflects a specific behavior of wages (Borrallo Egea and Río López 2021). Despite labor shortages and low unemployment, wage growth has been weak for many years, influenced by Japan’s labor market distortions (graph 7).

Graph 7: Wage growth in Japan

Historically, lifelong employment and seniority-based pay emerged as common practice in large Japanese firms, under the pressure of trade unions and facilitated by Japan’s high-growth period (Moriguchi and Ono 2004). There is no statutory law that guarantees lifetime employment, yet several court decisions in favor of the latter, including for nonunion employers and smaller firms, together with government interventions to subsidize jobs, in particular for older workers, have turned expectations of employment security into social norms. Today, Japan has a dual labor market, with most workers having regular full-time contracts and favoring long-term job stability over demands for salary increases. As a result, during the annual wage negotiations, trade unions focus more on realized rather than expected inflation.

The seniority-based pay makes it difficult for midcareer workers to move to another company, which would likely result in wage losses. As employees get older, their wages tend to rise above their productivity, which forces firms (more than 80 percent currently) to set mandatory retirement at sixty years (Organisation for Economic Co-operation Development 2019). Afterwards, most senior employees are rehired on nonregular contracts at significantly lower wages, which also dampens the pay for young people in nonregular employment. Japan’s rigid employment and pay system reduces not only labor mobility and productivity, but also inflation pressures from wage demands.

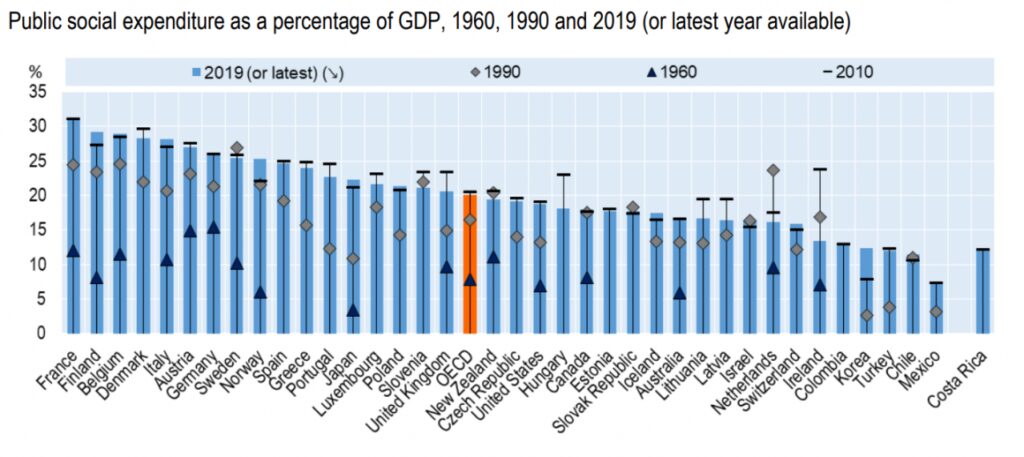

According to the Bank of Japan’s Tankan survey (or Short-Term Economic Survey of Enterprises in Japan), there has also been a broad decline in the firms’ short- and long-term inflation expectations from 1.5 percent to 1 percent in recent years (Borrallo Egea and Río López 2021). This is mainly due to weak consumer demand, which motivated firms to try to cut costs and limit price increases. Finally, another factor reducing inflation pressures is Japan’s leaner welfare system, which reduces the scope for the monetization of large social outlays. Despite its aging problem, public social spending, at about 22 percent of GDP, is much lower than the that of big European welfare spenders such as France, Finland, Denmark, and Belgium, at around 30 percent of GDP (graph 8). This reflects both lower social benefits and pensions where the replacement rate from mandatory schemes is only about 37 percent for a full-career average-wage worker, relative to the OECD average of 59 percent (OECD 2019).

Graph 8: Public social spending

Conclusion

Japan has been considered a leading example by modern monetary cranks of how running the printing press to monetize large-scale budget deficits is not likely to end up in high inflation. Yet they have not understood the fundamental and specific reasons why inflation in Japan has remained feeble during three decades of dismal economic performance. The recent spike in consumer price index inflation in the US and many other countries is clear proof that Japan has been a wrong example all along.