In the latest ranking of the world’s largest arms-producing and military services companies (the SIPRI Top 100), published in December 2022, two firms based in the United States—Peraton and Amentum—had recently been acquired by private equity firms. Both their arms sales were considered to have a high degree of uncertainty.

A growing number of arms producers and military service providers are being acquired by private equity investors, which are not subject to the same public financial reporting obligations as publicly listed companies. This trend is not unique to the arms industry—indeed, the arms industry is coming rather late to the private equity party—but it has important implications for scrutiny of a sector that is central to issues of peace and security.

Private equity firms invest capital raised from private investors. They use these funds to acquire stakes—often controlling ones—in other companies, with the aim of increasing the acquired company’s value and selling it on for a profit. Unlike public companies, private equity firms in the USA are not registered with the governmental financial watchdog, the Securities and Exchange Commission, and are not required to publish annual reports on or submit financial statements for any of the companies in their portfolios. Such firms enjoy similar exemptions in many other regulatory systems. This blog explores the increasing trend for private equity deals in the arms industry in the USA—the country with the largest number of companies in the SIPRI Top 100—and the implications for transparency.

Private equity and the arms industry

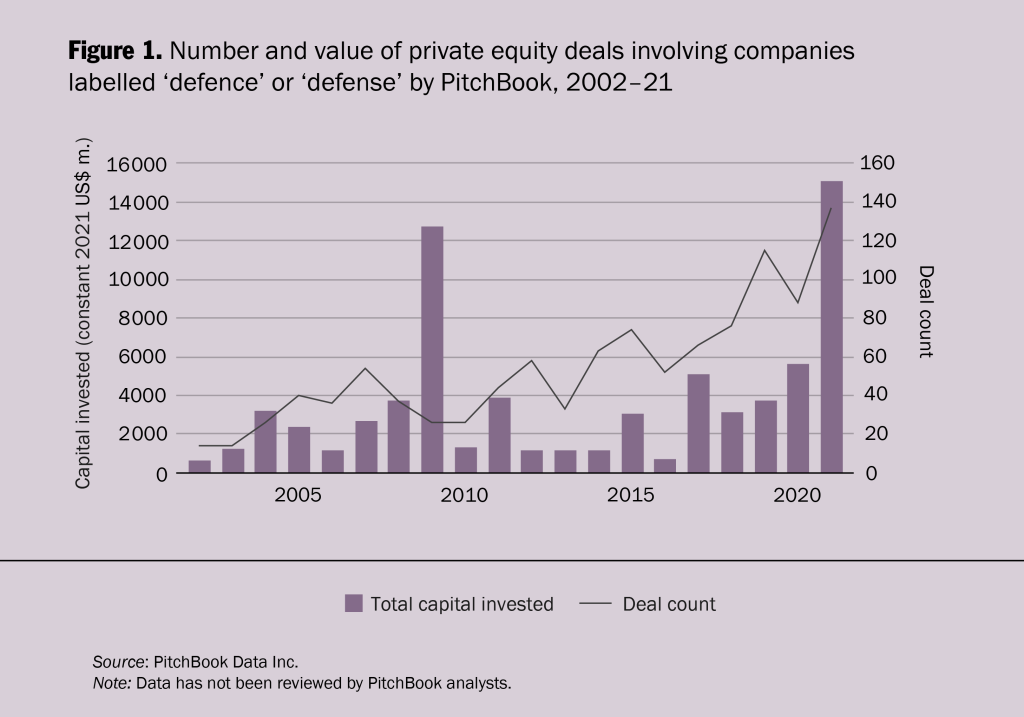

The involvement of private equity in the US arms industry rapidly expanded in the early 2000s when the US-led invasions of Afghanistan and Iraq raised the prospect of sustained high demand. Data extracted from PitchBook’s database of company mergers and acquisitions highlights that around 3700 US-based arms companies were involved in market deals in 2000–21. Of these, roughly 25 per cent were funded by private equity.

The number of private equity deals recorded by PitchBook has grown significantly since 2016 (see figure 1), as more funds enter the market and there have been record amounts of cash to invest ($4.6 trillion in 2022, according to The Economist). The war in Ukraine and tensions across the Taiwan Strait are likely to drive demand for weapon systems for some time to come, making the arms sector even more appealing to investors, private equity included.

A closer look at two private equity acquisitions

Amentum was ranked 25th in the SIPRI Top 100 for 2021, with estimated arms sales—sales derived from the provision of military goods and services to military customers—of just over $5 billion. The company was created in early 2020 as a spin-off of AECOM’s management services business and acquired by the p∂rivate equity firms American Securities LLC and Lindsay Goldberg. Later that year, following patterns of sectoral integration characteristic of private equity acquisitions, Amentum added aerospace company DynCorp International (ranked 67th in the SIPRI Top 100 for 2020) to its broad portfolio of services including consulting, logistics, IT and training. In January 2022, Amentum expanded further by acquiring Pacific Architects and Engineers (ranked 93rd in the SIPRI Top 100 for 2021) for $1.9 billion. Amentum CEO John Vollmer claimed in 2022 that the company was now the second-largest provider of services to the US government. The company provides a ‘Year in Review’ document, but this has only five pages and does not disclose any financial information. A classic annual report is usually over 100 pages long and includes information on the overall situation of the company, such as profitability and employment levels, as well as forecasts, allowing assessment of its health status. The SIPRI estimate for Amentum for 2021 was therefore deemed to be the same ratio of arms sales to total sales as the previous year.

Peraton (ranked 21st in the SIPRI Top 100 for 2021, with arms sales of $5.8 billion) has been owned by private equity firm Veritas Capital since 2017. Peraton did not appear in the SIPRI Top 100 prior to 2021. However, Peraton’s acquisition of Northrop Grumman’s IT and mission-support services business for $3.4 billion in February 2021 and subsequent acquisition of Perspecta (another military-related IT services company) in May 2021 for $7.1 billion earned Peraton its place in the ranking for the first time. Like Amentum, no annual report was available and so the SIPRI estimate had to rely on the assumption that arms sales had grown by the same proportion of total sales had Peraton conducted the acquisitions in 2020.

However, the estimates made for both companies are valid only for a short time and, in the absence of new evidence, the data might soon be deemed out of date or become too unreliable for them to be included in the Top 100.

Private equity and transparency

In an industry that tends towards secrecy, public financial reports are one of the most important sources of information for those who want to observe industry trends and developments. As private equity firms are not required to publish such financial reports, and often sell the companies they acquire to other private equity firms, an arms company’s sales could be hidden from public scrutiny indefinitely—or at least until the company is acquired by a publicly listed company or makes an initial public offering (IPO).

The growth of private equity is far from the only challenge to arms industry transparency worldwide, but the fact that it is affecting the US industry on such a scale makes it significant. US companies have long dominated the global arms industry: the USA accounted for 40 of the companies in the SIPRI Top 100 in 2021 and $299 billion of the $592 billion of their total sales. Therefore, if data on the sales of major US companies is unavailable, it is harder to identify or predict overall industry trends.

There are other ways of ascertaining arms companies’ sales beyond public financial reports, but these are less reliable and sometimes not open source. Initiatives such as SIPRI’s Arms Industry Database rely on open-source information so that everyone, regardless of position or location, has free access to the underlying data and can test the analyses.

Since 2018, the reporting of at least 11 arms companies has been affected by private equity acquisition: AECOM, AllClear, AM General, Cobham, Cubic Corporation, DynCorp, MD Helicopters, Navistar Defense, Pacific Architects and Engineers, Peraton and Ultra Electronics. Some of these companies had previously been ranked in the SIPRI Top 100.

Looking ahead

It seems unlikely that private equity will become as active in the arms industry in other markets as it is in the USA. For example, an assessment by the consultancy firm KPMG suggests that the ‘fragmented’ arms market in Europe—where many companies are entirely or partly state-owned—could deter private equity investors. Nonetheless, US private equity firms have acquired several European arms companies, such as the United Kingdom’s Cobham and Ultra Electronics. The same report encourages investors to consider the scaling opportunities offered by entities such as the Five Eyes (Australia, Canada, New Zealand, the UK and the USA) to leverage their common standards and procurement procedures.

In the USA, the trend towards private equity acquisitions seems to be gathering steam. In Pitchbook’s 20-year data set, 21 per cent of defence-related private equity acquisitions occurred in 2020 and 2021. While rising interest rates might make leveraged buyouts less appealing, the continued economic fallout of the Covid-19 pandemic and related supply chain disruptions could make arms companies easy prey for private equity firms. The US Department of Defense is also making large sums available to fund research and development into new weapon technologies, which makes the industry an even more desirable target for private equity investors.

The current regulatory framework for private equity and the growth of private equity in the arms industry make it harder to get a clear picture of how the industry is evolving, in the USA and beyond. This restricts oversight and accountability of this critical sector and hampers informed policymaking.