Sanctions have not breached Russia’s economic fortress, but they have put a time bomb under its foundations.

In the 18 months for which Russia has been waging war against Ukraine, Western countries have imposed more than 13,000 sanctions on Russia — yet the Russian economy shows no sign of collapsing. On the contrary, the International Monetary Fund forecast for the country is for 1.5% growth this year — more than the economies of Germany or the UK.

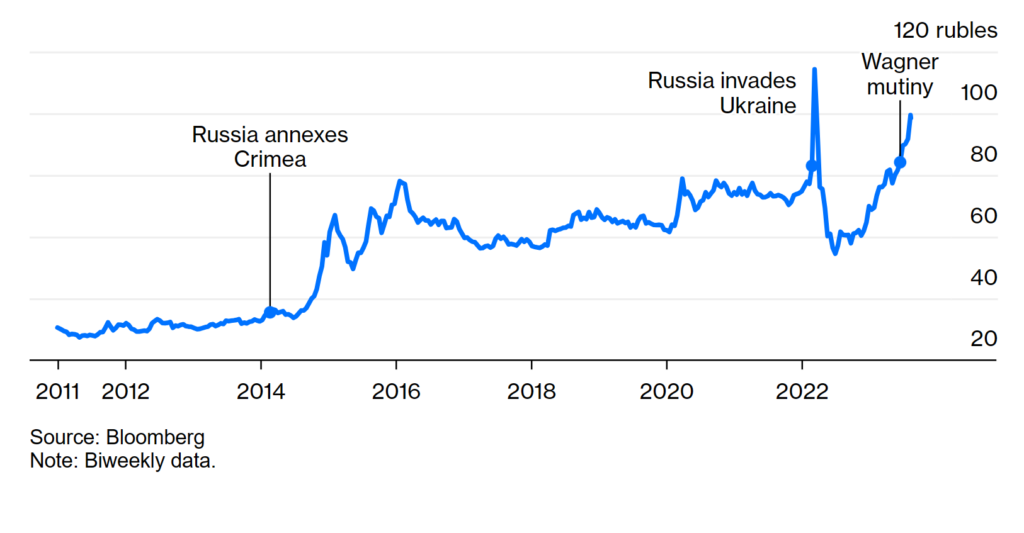

The Kremlin likes to boast that sanctions don’t work, and similar reservations are increasingly being expressed by Western observers. Yet the rapidly depreciating ruble, which in August became the worst-performing currency among developing countries, suggests otherwise. The Bank of Russia was even forced to hike the key rate to 12% from 8.5% in one day during an emergency meeting on Aug. 15. This move is likely aimed at taming inflation that will be fueled by the ruble’s weakening.

While one shouldn’t expect this to force Vladimir Putin to stop his disastrous war, sanctions pressure has proven efficient for at least one goal: reducing the flow of funds to the Russian economy. The Kremlin has no other option than to divert money to the war machine, putting the economy on increasingly unsustainable footing. So the West should continue to go after the Kremlin’s revenue sources, including by lowering the oil price cap, introducing similar measures on other Russian exports, and closing sanctions loopholes.

The fluctuating ruble rate (from 53 to the dollar in June 2022 to 100 a year later) is indeed an indicator of deeper problems. The immediate trigger for the ruble’s nosedive in July was almost certainly the brief mutiny staged in late June by Yevgeny Prigozhin and his mercenary army, Wagner, which added internal instability — something that hadn’t seriously impacted the ruble exchange rate since the mass street protests of 2011-2012 — to the risks facing Russia and impacting on the rate.

How Many Rubles One Dollar Buys

Russia’s currency has weakened considerably ever since its annexation of Crimea

But the fundamental reasons for the fluctuating ruble rate are linked to changes in the structure of market demand, above all reduced revenues from exporting oil and gas due to the EU embargo on importing Russian oil and oil products, the price cap imposed by the G7, and the subsequent rerouting of those commodities to different destinations.

Although Russia has managed to redirect significant volumes of its oil from Europe to Asian markets, the transactional costs have increased, and there is no substitution for the European gas market. The likelihood of the price cap being lowered even further and stricter enforcement of sanctions compliance means the prospects for Russian exports are dismal. Even if the Russian economy looks confident right now, in the medium-term, the decline in export revenues will lead to an even greater weakening of the ruble and, as a consequence, inflation.

The ruble is replacing foreign currencies in export revenues, and now accounts for 39%, reducing the net inflow of foreign currency into the country. There is also an imbalance in demand for currencies: exporters need Chinese yuan, while importers want dollars and euros. In previous years, when the ruble dropped significantly in value, foreign funds and global investment banks sprang into action to profit from the situation. Their presence also evened out market fluctuations. Now they are gone, and that means future swings in the exchange rate are guaranteed. This increased volatility weakens the currency’s payment and saving functions: People and businesses will cut costs and postpone investments.

Of course, Putin can always resort to his previous tactic of calling Rosneft Chief Executive Officer Igor Sechin and other exporters and demanding that they repatriate hard currency. But manually managing the ruble rate will not fundamentally resolve the situation.

The ruble’s main adversary is the Russian state itself, which is actively spending budget funds. Its high volatility and the fact that it halved in value in less than a year are consequences of the new economic policy forged by the war and sanctions. What the Kremlin calls the “structural transformation of the economy” is more commonly known as military Keynesianism: boosting economic growth through increased military spending.

The “structural transformation” of the economy effectively amounts to a huge increase in defense spending. As in Soviet times, war has engendered entire groups of beneficiaries: the military-industrial complex and related manufacturing, as well as military personnel and their families, who are part of the state sector.

Defense spending rose 9.2% in 2022 to $86.9 billion, according to estimates by SIPRI. In this first half of this year, it was already way over budget, standing at more than $72.2 billion. Combined with social spending (for which over $75 billion was budgeted this year), that makes up more than one-third of all state spending — twice as much as before the war.

The defense industry is pulling other industries along with it, propelling demand for imports, sustaining GDP and putting money in ordinary Russians’ pockets. Real incomes increased in regions that are home to military manufacturing, according to the state statistics service, and where there are reportedly high numbers of professional soldiers, such as Chechnya. The defense industry is working around the clock, luring personnel away from the civilian sector with high salaries and exemptions from being mobilized. To retain personnel, other sectors are also having to raise salaries. The groundwork for runaway inflation has been laid.

A significant part of both state and individual spending is on imports, and the return of Russian imports to their pre-war level is stimulating demand for hard currency. Until the government cuts or slows down spending that stimulates imports, the ruble exchange rate will remain weak.

Trust in the Russian financial system is dwindling fast, as evidenced by the constant outflow of capital. Hard currency deposits into Russian banks fell by $9.1 billion to $152.4 billion in June, while from the beginning of 2022 to May 2023, the volume of deposits abroad made by Russians (mostly in Armenia, Georgia, and Kazakhstan) grew by $43.5 billion.

There is no help forthcoming for the ruble. The central bank’s freeze on buying hard currency from August through the end of the year is more of a palliative measure than anything else.

Putin’s disastrous war against Ukraine and the ensuing sanctions have not breached Russia’s economic fortress, but they have put a time bomb under its foundations. Any decrease in market demand looks unlikely while the war rages and the country is gearing up for presidential elections. Thanks to sanctions, the country is unable to produce certain complex hi-tech goods itself, meaning that far from becoming more self-sufficient, Russia’s dependence on imports will only grow.

The volatile and weakening ruble exchange rate is testament to just how imbalanced the Kremlin has allowed the economy to become, and that it is already barely coping. When the war ends, the sudden switch in demand from the inflated defense sector back to the civilian sector will be a powerful shock that will be impossible to absorb painlessly. As we know from history, it also proved impossible for Russia’s predecessor, the Soviet Union.