The continued use of shadow fleet and transshipment networks allow sanctioned countries to bypass energy sanctions, underscoring the need for stronger and more unified enforcement.

Intensifying competition among sanctioned oil exporters for a shrinking pool of buyers drove steep discounts in 2025, enabling China to save up to $28.8 million per day on imports at peak discount levels.

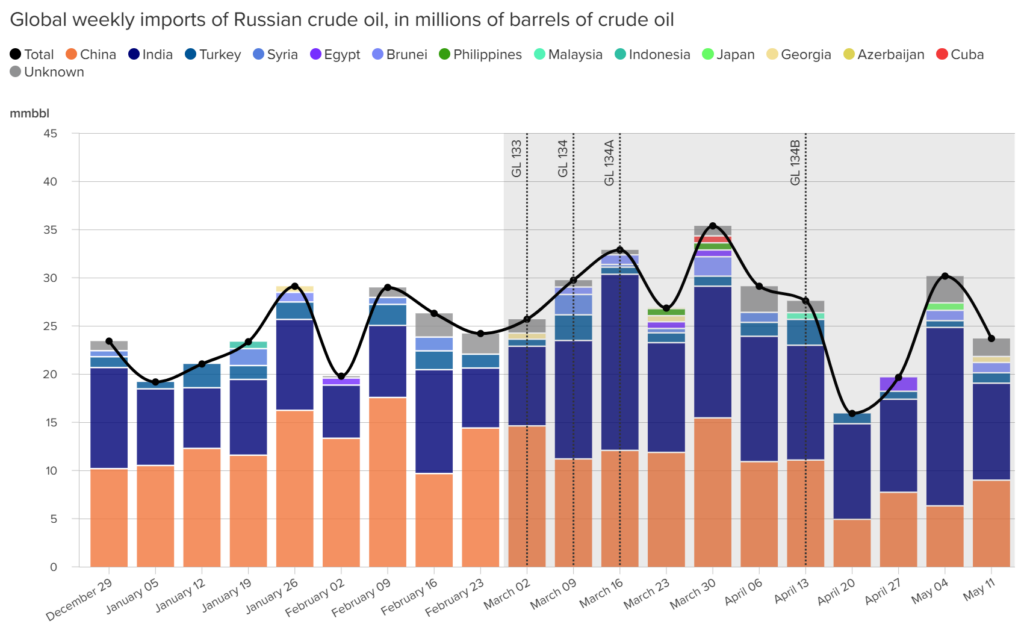

US sanctions waivers, rising oil prices, and supply shortages following the conflict in Iran have boosted demand for Russian crude. Since the waivers were issued, Russia has supplied approximately 300 million barrels to the international market as of May 11, with India re-emerging as a major importer and Southeast Asia emerging as a new destination for Russian crude.

Three of the most heavily sanctioned regimes in the world—Iran, Russia, and Venezuela—also happen to be major players in the global energy market. The United States and its allies have levied major sanctions and other restrictive economic measures on these regimes’ crude oil exports to disrupt, deter, or deny them from funding activities that threaten US and allied national security interests and foreign policy goals.

However, the use of sanctions and economic statecraft tools comes at a cost and often has unintended consequences. Sanctions against major oil-producing countries have led to realignment of global crude oil trade routes and the emergence of the global shadow fleet of tankers.

The Atlantic Council’s Energy Sanctions Dashboard, created by the Economic Statecraft Initiative and Global Energy Center,

1) assesses how sanctions have impacted global crude oil flows,

2) explores the unintended consequences for the global crude oil industry, and

3) analyzes lessons learned about the deployment of energy sanctions for achieving foreign policy objectives.

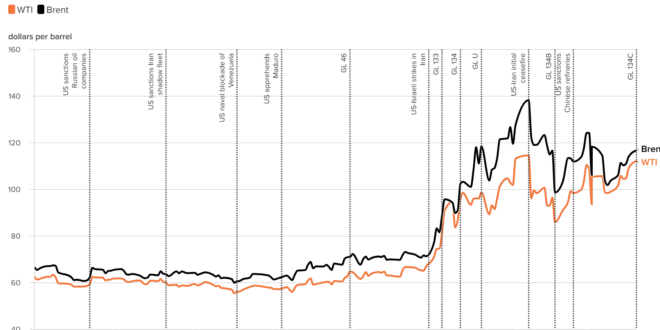

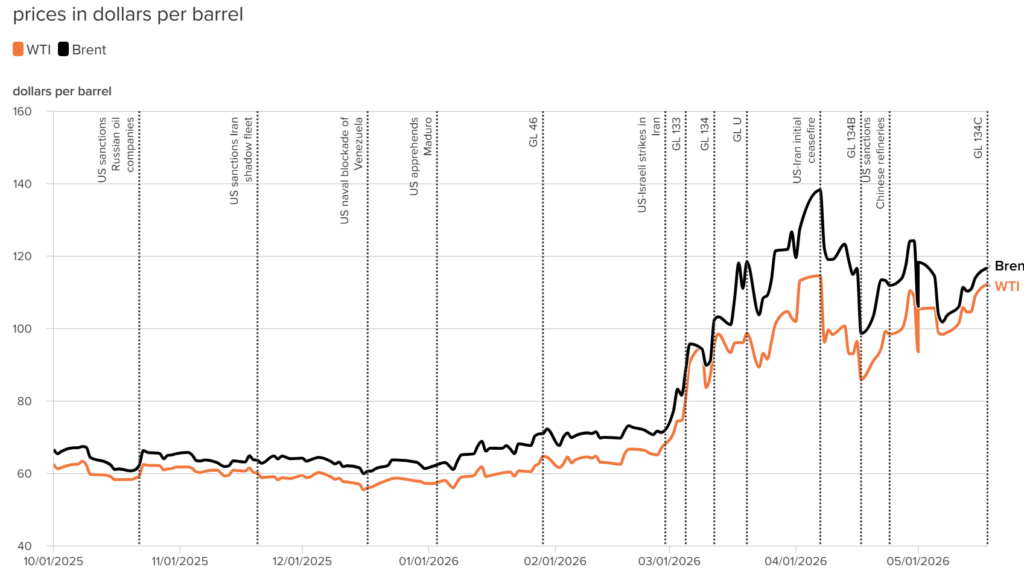

The largest disruption to global energy flows in history also disrupted the global energy sanctions regime in the first months of 2026. Can US sanctions waivers offset the supply shock from the effective closure of the Strait of Hormuz? And how can US policymakers stabilize energy markets without weakening sanctions pressure on Russia and Iran? This edition of the Atlantic Council’s Energy Sanctions Dashboard explores these questions and more.

Much has changed in the energy sanctions world since the launch of this dashboard in October 2025. In Venezuela, a US oil blockade intensified pressure on the Maduro regime ahead of his capture in January 2026, followed by general licenses that redirected some crude flows toward the United States. In the Middle East, conflict with Iran and disruptions in the Strait of Hormuz—through which roughly 20 percent of global oil passes—have significantly constrained shipments to Asia and Europe.

Amid these disruptions, Washington eased restrictions on certain Russian and Iranian crude to mitigate supply shocks, particularly for India and other Asian buyers. However, these moves have drawn criticism for boosting revenues for sanctioned regimes.

At the time of writing, the Iran war and disruptions to shipping through the Strait of Hormuz are ongoing, and the timeline and terms of any US-Iran peace deal remain uncertain. Even after a potential agreement, restoring damaged or disrupted oil production and export capacity across the region could take months. This will likely tighten global supply in the near term and increase the relative economic leverage of Russia and Iran.

2025 energy sanctions: How shadow fleet undermined energy sanctions enforcement

Despite multiple geopolitical crises in 2025, including the initial US-Israeli strikes on Iran during the Twelve-Day War in June and increased attacks on energy infrastructure in the Russia-Ukraine war, global crude markets remained in a state of oversupply, with oil prices declining over the course of the year. The decisions by OPEC+ to boost output throughout the year, which reversed multiple years of voluntary production cuts, were a major factor behind this trend. Due to weak sanctions enforcement, Russia remained one of the world’s top oil suppliers, accounting for 8.1 percent of global crude exports alone in 2025. Iran added an additional 3.9 percent while Venezuela made up 1.8 percent, meaning that the three sanctioned countries together accounted for almost 14 percent of global oil shipping flows, according to data from Kpler.

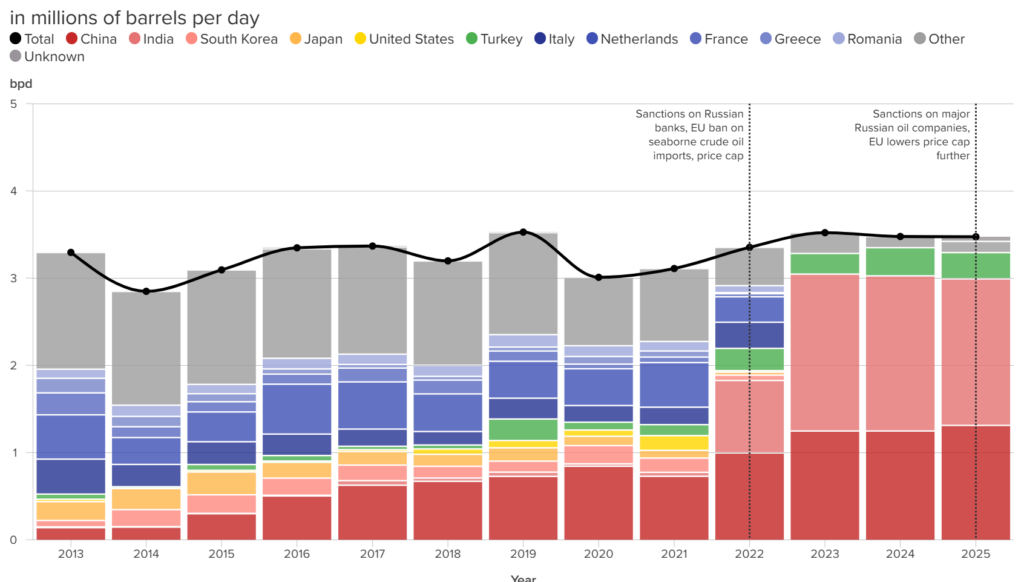

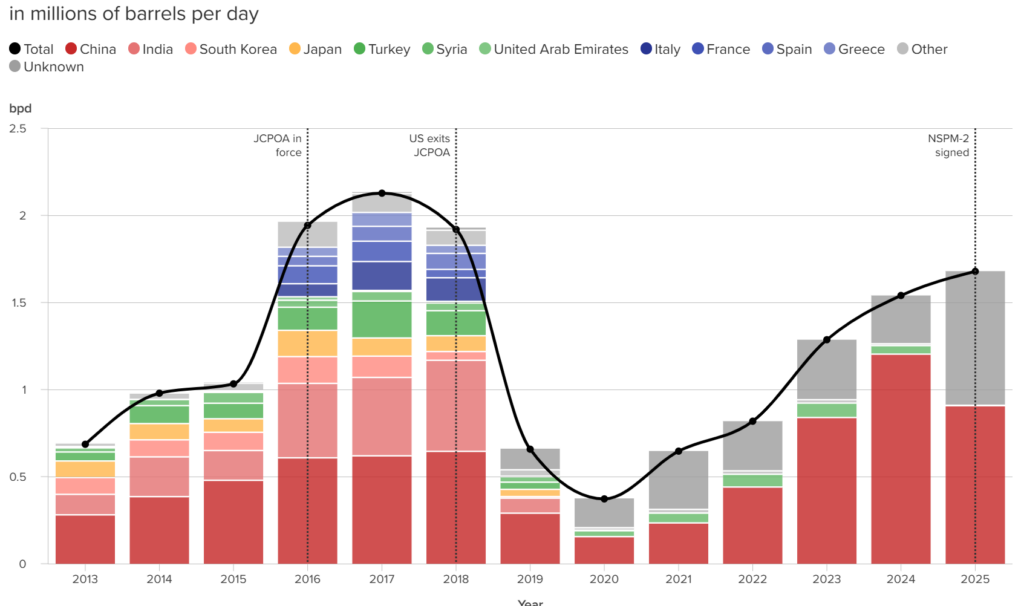

Following Treasury’s designation of Lukoil and Rosneft in October 2025 and the subsequent UK and EU sanctions, Chinese state-owned oil majors initially suspended Russian oil purchases. However, the data shows that China has continued buying significant amounts of Russian oil, suggesting that imports have shifted to smaller refiners in an effort to protect larger refiners from secondary sanctions risks. Chinese imports of Venezuelan oil also rose significantly in 2025. This came after the US ramped up pressure on Venezuela and the Treasury Department’s Office of Foreign Assets Control temporarily revoked Chevron’s general license. Due to Venezuela’s increased economic isolation, China was likely able to import Venezuelan crude at a significant discount during this period. Finally, while Chinese imports of Iranian oil appear to have dropped, imports by unknown buyers increased substantially in 2025. Given that there are few other known importers of Iranian oil, it is reasonable to assume that a large portion of the unknown imports are also headed to China, albeit through obscure means.

Growing economic pressure, a shrinking customer base, and intensifying competition among sanctioned exporters have forced Iran, Russia, and Venezuela to export crude at steep discounts. Throughout 2025, these reached as much as $10 to $15 per barrel. Based on export volume data, our calculations indicate that, at peak discount levels, China saved up to $28.8 million per day by importing sanctioned crude. Since the outbreak of the Iran conflict, however, rising oil prices, supply uncertainty, and the issuance of sanctions waivers has drastically narrowed these discounts and sometimes even generated premiums. While Iran has seen slight premiums, Russia has been the real winner, with crude trading at premiums of up to $10 over ICE Brent. This highlights how sanctioned exporters stand to benefit if the Iran conflict—and the resulting supply uncertainty—continues to drag out.

To evade detection, these sanctioned countries relied on transshipment—the ship-to-ship transfer of sanctioned crude cargoes to “unsanctioned” ones—or by re-exporting through third countries to obscure cargo origins. Central to this is the use of shadow fleet: vessels with opaque ownership structure that evade tracking by disabling AIS devices or spoofing their location signals. Despite growing Western efforts to sanction and even seize these ships, the fleet continues to operate relatively unencumbered. To improve the effectiveness of energy sanctions, not only do these sanctions need to be more strictly enforced, but Western partners also need to coordinate their sanctions to ensure that there is coherence in the vessels that are being targeted.

On the demand side, China spent much of 2025 aggressively stockpiling oil. Last year, China’s crude imports reached 11.6 million barrels per day—up from 11.1 million in 2024—with over 22 percent consisting of sanctioned crude. Heavy reliance on imported oil and rising geopolitical risks have driven China to aggressively stockpile oil as part of its energy security strategy, adding at least 169 million barrels of storage across eleven sites in 2025 and 2026, and storing approximately 83 percent of its import increase in 2025. However, China’s long-term demand for oil should not be overstated. Stockpiling risks obscuring a broader trend of slowing demand growth, as China accelerates its energy transitions—with 2024 estimates suggesting that over 30 percent of China’s electricity is already generated through wind, solar, and hydropower. For sanctioned exporters, this compounds an existing challenge: growing competition among sanctioned crudes has already forced deep price discounts, a pressure likely to intensify as Chinese demand plateaus. Nevertheless, as the Iran conflict continues to shape the energy market, China’s demand for crude oil—sanctioned or not—will remain a key factor shaping its trade relationships with sanctioned regimes in the near term.

From 2023 to 2025, Russia rerouted crude oil exports to the Chinese and Indian markets

Much of Iran’s sanctioned oil has been pushed to buyers in the global shadow fleet

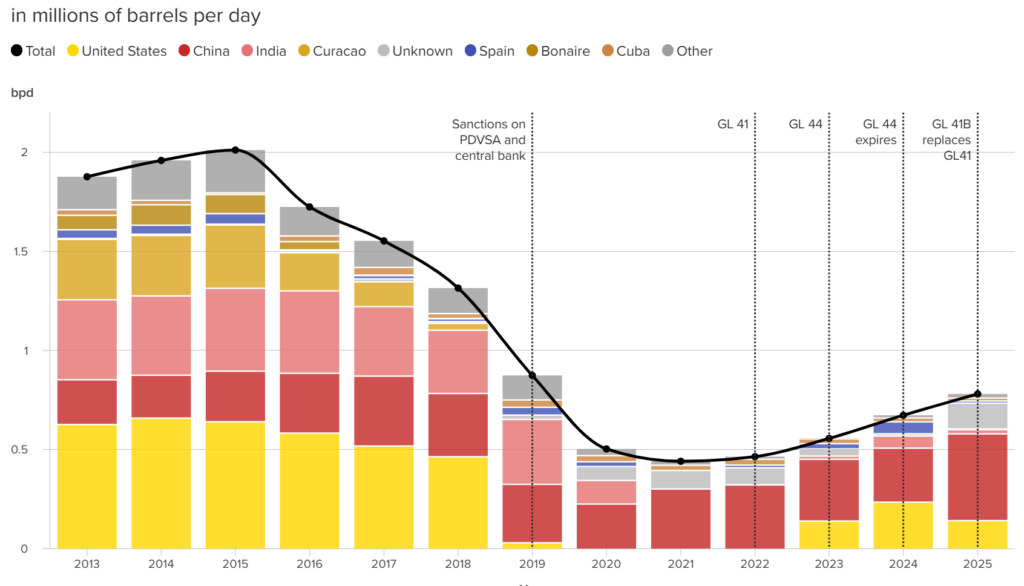

The Chinese market has emerged as the primary destination for Venezuela’s crude oil

2026 updated: Expanded client base for sanctioned crude

As significant volumes of oil were removed from the global market due to the effective closure of the Strait of Hormuz, countries started seeking alternatives to Gulf supplies. To help ease the shortage of oil, the United States issued sanctions waivers to allow countries to temporarily import crude oil from Russia to replace barrels that would normally come from the Gulf. The two initial waivers expired on April 4 and 11. Soon after, Bessent announced the United States would not renew the waivers, but reversed course and issued a new waiver on April 17—which has been extended again.

The Trump administration set the first round of waivers as narrowly tailored measures that would only cover oil already loaded on tankers. The waivers allowed imports of Russian crude to rise approximately 41 percent in March over the previous month, reaching a level not seen even before Russia’s full-scale invasion of Ukraine in 2022 or Crimea in 2014.

Major geopolitical events of 2026 led to dramatic changes to sanctions regimes and oil prices

India has resurfaced as a major importer of Russian crude following the issuance of the waivers, replacing supplies previously sourced from the Gulf and returning to import volumes comparable to those seen prior to the sanctioning of Russian oil majors. At the same time, Southeast Asia, which has been one of the hardest-hit regions in this energy crisis thus far, has emerged as a new destination for sanctioned Russian crude. In late March, the Philippines became the first country in the world following the Strait of Hormuz’s blockage to declare a national energy emergency. The archipelagic nation, which imported over 96 percent of its crude oil from the Middle East in 2025, is particularly vulnerable to the crisis and has already seen diesel and gasoline prices double in the first month of the conflict. Other countries in the region, such as Thailand and Vietnam, also rely on imports for 70 percent or more of their energy needs, heightening fears of an energy shortage. While imports into the region have remained modest—totaling roughly eight million barrels since the waivers were introduced, as of May 11, 2026—mounting energy pressures are driving governments to consider Russian supplies more seriously.

Since the issuance of the waivers, Russia has supplied approximately 300 million barrels of oil to the international market as of May 11, 2026, according to our calculations. This supply helped provide additional temporary relief from the strait’s blockage, but it also comes with risks. As supply from the Middle East remains limited, the use of sanctions waivers could unintentionally encourage new dependencies on Russia—and potentially undermine the effectiveness of sanctions on Russia following the expiration of the waivers.

Countries snap up Russian crude oil during sanctions waiver periods

India recently advocated for an extension of the waiver, as it continues to face extreme supply shortages. But it might not matter either way. In the long term, constrained global oil supply could also incentivize countries to continue importing Russian crude despite sanctions—accepting the risk of financial penalties rather than facing the economic consequences of significant domestic energy shortages. Officials at India’s Petroleum Ministry have already expressed willingness to import Russian oil irrespective of waivers.

Countries in Southeast Asia may also continue importing Russian oil to reduce the risk of relying on the Middle East. Following Indonesian President Prabowo Subianto’s meeting with Russian President Vladimir Putin in Moscow on April 13, Indonesia announced that it will begin importing Russian crude to further diversify its supply. Countries such as Thailand, Malaysia, Vietnam, and Sri Lanka have also scrambled to negotiate with Russia for shipments of oil and petroleum products over the past few months.

Meanwhile, buyers have taken a more cautious approach towards Iranian oil. While the United States issued a waiver permitting the sale of certain barrels of Iranian crude, the financial, logistical, and legal risks associated with Iranian crude have deterred otherwise eager buyers. Following the expiration of the Iran sanctions waiver, the United States returned to its strategy of “maximum pressure” against Iran’s economy as part of the Department of the Treasury’s “Operation Economic Fury”. The operation marks an escalation in the US sanctions strategy, using secondary sanctions to target shadow fleets, foreign refiners, maritime and financial intermediaries, and overseas commercial and banking infrastructure, including intermediaries in China, the United Arab Emirates, Hong Kong, Iraq, and Oman. In response, China ordered its companies not to comply with US sanctions against Chinese refineries, deploying its “prohibition order” for the first time. The move marks a shift in Beijing’s response to US sanctions, from one where China would have rhetorically condemned US trade restrictions while allowing companies to comply, to a more confrontational approach.

How to preserve the power of US energy sanctions and counter adversaries

To preserve energy sanctions as an effective tool of economic statecraft against Russia and Iran, the United States should focus on targeting two central elements of sanctions evasion networks: shadow fleet tankers and Chinese “teapot” refineries. These elements have facilitated Russia-Iran-China oil trade for years and were notably analyzed by Kimberly Donovan and Maia Nikoladze in their March 2024 “Axis of Evasion” article.

Targeting these networks has become a core element of the Economic Fury strategy. Recently, the US Treasury’s Financial Crimes Enforcement Network (FinCEN) issued an advisory to financial institutions outlining red flags associated with Iranian oil smuggling, including shipping activity, irregular shipping documentation, and vessels that frequently change names. The advisory underscores the increasingly important role of financial institutions and the private sector in enforcing US energy sanctions.

The Treasury Department has also designated several Chinese teapot refineries for purchasing Iranian oil. Sustained enforcement against these entities will be critical to maintaining pressure on Iran and disrupting trade flows that weaken US and allied sanctions regimes.

At the same time, enforcement against Russia should not recede amid heightened focus on Iran. While the current energy crisis in South and Southeast Asia may complicate the removal of Russia oil waivers, the United States and its allies could still tighten pressure by lowering and more rigorously enforcing the G7 oil price cap, potentially closer to the $44 level adopted by the European Union.